Zero Based Budgeting for Teenagers Explained Simply means deciding where every single dollar goes before you spend it — so money stops disappearing and starts working for you. This simple system helped me go from constantly feeling broke to feeling confident, calm, and in control of my money. I didn’t earn more, I just learned how to give my money purpose — and that changed everything.

If you want a formal definition, zero-based budgeting is explained clearly here on Investopedia

I wasn’t bad with money because I was irresponsible. I was bad with money because no one ever taught me how it actually works. What follows isn’t a textbook explanation. It’s my real story — mistakes, frustration, breakthroughs — and a simple system that finally made money feel clear, calm, and empowering.

Zero Based Budgeting for Teenagers Explained Simply: Why It Finally Made Sense to Me

I still remember opening my banking app at 17 and feeling that familiar pit in my stomach.

I had a part-time job. I didn’t have rent. I didn’t have bills.

So why was my balance always close to zero?

Every paycheck followed the same pattern:

- First few days: freedom

- Next week: confusion

- End of the month: panic

Money wasn’t gone — it had just leaked away quietly. Snacks after school. A game download. Random online purchases. None of it felt big enough to worry about… until it all added up.

The emotional part surprised me most. I didn’t feel lazy or careless. I felt out of control. And that feeling followed me everywhere.

That’s when I learned the most important lesson of all:

Money problems are rarely about math. They’re about clarity.

What Is Zero Based Budgeting (In Teen Language)?

Let’s strip away the intimidating finance words.

Zero-based budgeting simply means this:

You decide where every dollar goes before you spend it — until your balance hits zero.

Important clarification:

“Zero” doesn’t mean you spend everything.

It means every dollar is assigned a purpose.

Some dollars go to:

- Spending

- Saving

- Giving

- Future goals

When the money arrives, you tell it where to go. Not the other way around.

For the first time, I wasn’t reacting to money.

I was directing it.

The Moment It Finally Clicked for Me

The breakthrough didn’t happen in a classroom. It happened at my desk, late at night, with a cheap notebook and a pen.

I wrote down:

- My monthly income

- Every place my money could go

Then I did something radical for a teenager:

I planned my spending before I had the money.

That single moment changed everything.

Suddenly:

- I stopped feeling guilty when I spent

- I stopped feeling anxious checking my balance

- I stopped guessing and started choosing

Zero-based budgeting gave me something I’d never had before — permission with boundaries.

How Zero Based Budgeting Actually Works (Step by Step)

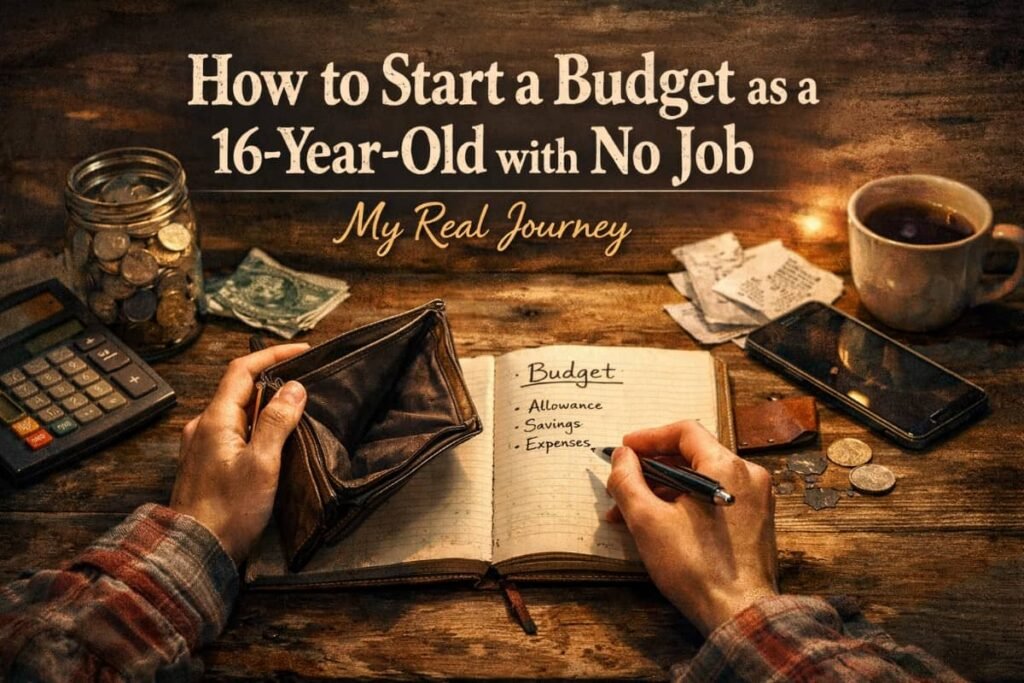

Step 1: Know Exactly How Much Money You Have

This includes:

- Allowance

- Part-time job income

- Gift money (if regular)

Use the lowest predictable number. Overestimating is how budgets fail.

Step 2: List Your Real-Life Categories

Forget complicated charts. Mine looked like:

- Snacks & food

- Entertainment

- Transport

- Saving

- Fun money

- Gifts

The rule: If you spend it, it gets a category.

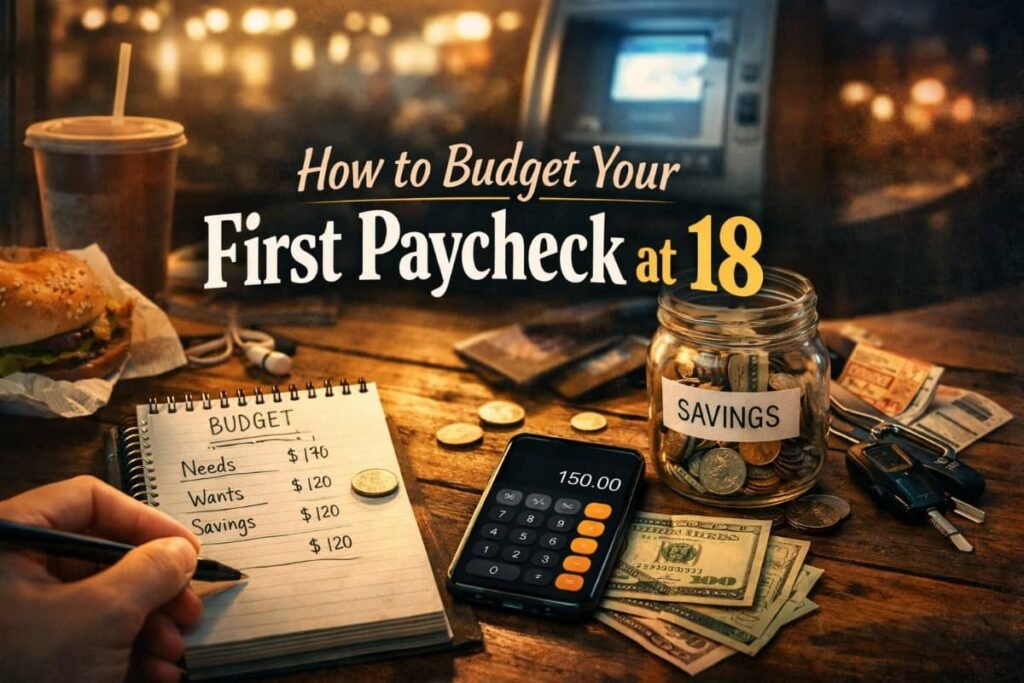

Step 3: Assign Every Dollar a Job

If you earn $200:

- $60 snacks

- $40 entertainment

- $50 savings

- $30 transport

- $20 fun buffer

$200 – $200 = zero

No unassigned money = no mystery stress.

This idea of assigning every dollar a purpose is also echoed in basic budgeting guidance from MoneyHelper’s official budgeting advice in the UK

Step 4: Track Gently, Not Obsessively

I didn’t log every cent. I checked weekly.

Progress beats perfection every time.

Why This Method Works So Well for Teenagers

Teen life is unpredictable. Schedules change. Friends invite you out at the last minute. Impulse buys happen.

Zero-based budgeting works because it’s flexible but intentional.

You’re not saying “I can’t spend.” You’re saying, “I already decided.”

That mindset shift is everything.

Even government education programs now emphasize early money habits — the Consumer Financial Protection Bureau’s teen money resources reinforce why learning budgeting young builds lifelong confidence

How Zero Based Budgeting Helped My Confidence (Not Just My Wallet)

Here’s something no one talks about:

Money clarity builds self-trust.

When I followed my budget:

- I felt mature

- I felt capable

- I felt proud

I stopped hiding purchases. I stopped avoiding my balance. I stopped feeling behind.

Confidence doesn’t come from having more money. It comes from knowing what you’re doing with what you have.

Common Mistakes Teens Make (I Made Them All)

1. Being Too Strict

If you don’t allow fun money, the budget collapses. Fun isn’t the enemy. Guilt is.

2. Forgetting Irregular Expenses

Birthdays. School events. Random costs. Build a “future stuff” category.

3. Giving Up After One Bad Week

One mistake doesn’t mean failure. It means learning.

Budgeting is a skill — not a personality trait.

Australian youth finance programs agree that mistakes are part of learning — ASIC MoneySmart’s budgeting guides emphasize adjusting instead of quitting

How Parents Can Support Without Controlling

If you’re a parent reading this, here’s the truth:

Control creates rebellion. Guidance builds confidence.

What helped me most wasn’t rules. It was a conversation.

Helpful support looks like:

- Asking questions, not giving lectures

- Letting teens make small mistakes

- Celebrating effort, not perfection

Money habits stick when teens feel respected.

Real-Life Example: My First Savings Win

Three months into zero-based budgeting, something wild happened.

I had money left over.

Not accidentally. On purpose.

I saved for something specific — no borrowing, no stress.

That moment taught me:

Planning feels better than impulse, every time.

Why Schools Don’t Teach This (And Why That’s Okay)

Most schools teach math. Few teach money behavior.

That gap isn’t your fault.

The good news? You don’t need a class. You need a system — and practice.

Zero-based budgeting is simple enough to learn young and powerful enough to last a lifetime.

How to Start Today (Even If You’re Overwhelmed)

Start messy. Start small. Start honest.

All you need:

- One page

- One income number

- A few categories

You don’t need perfection. You need clarity.

Frequently Asked Questions (FAQs)

1. Is zero based budgeting too complicated for teenagers?

No. It’s actually simpler than traditional budgeting because it removes guesswork.

2. Do I need an app to use zero based budgeting?

No. Paper works. Notes apps work. Apps are optional — clarity is not.

3. What if my income changes every month?

Budget based on the minimum you expect. Adjust when extra comes in.

4. Can zero based budgeting help with saving?

Yes — saving becomes intentional, not accidental.

5. How long does it take to see results?

Most teens feel calmer within the first month. Confidence builds fast.

Read Also: From Broke to Building My Dreams: 15 Pocket Money Hacks Every Student Must Know

Final Thoughts: Why I Wish I’d Learned This Earlier

If I could go back and tell my teenage self one thing, it would be this:

Money isn’t scary when you give it direction.

Zero Based Budgeting for Teenagers Explained Simply isn’t just about dollars. It’s about freedom. Confidence. Choice.

And the best part?

You don’t need more money. You just need a plan.

If you’re a teenager reading this — or a parent guiding one — start today. One page. One decision. One step toward a calmer financial future.

You’ve got this.